Like an unstoppable energizer, Oracle’s Fusion Cloud Applications business posted a 13% growth in revenues in its latest quarter while taking a contrarian view on the Cloud applications market meltdown speculation.

Oracle chairman and CTO Larry Ellison reiterated his exceptionalism that the vendor’s illustrious history – coupled with its comprehensive product offerings and vast installed base – will insulate itself from any external shock to any part of its business whether real or imagined.

Ellison’s conviction stems from three attributes that have manifested over the past few years. First, without relying on acquisitions, much of Oracle’s Cloud applications revenues have been growing steadily and consistently through organic means.

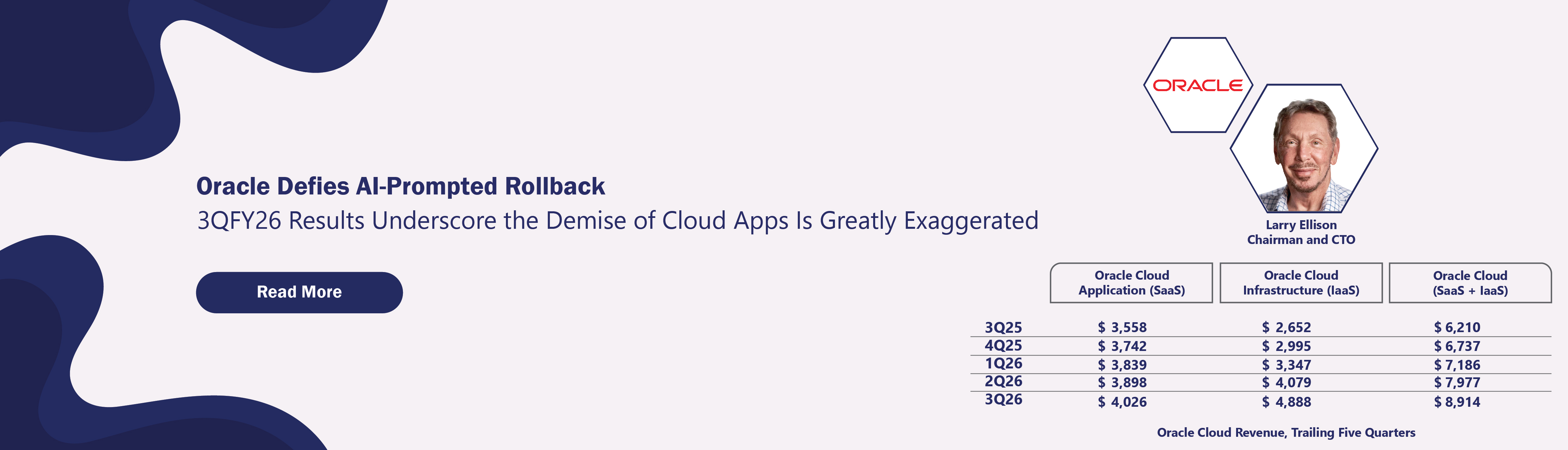

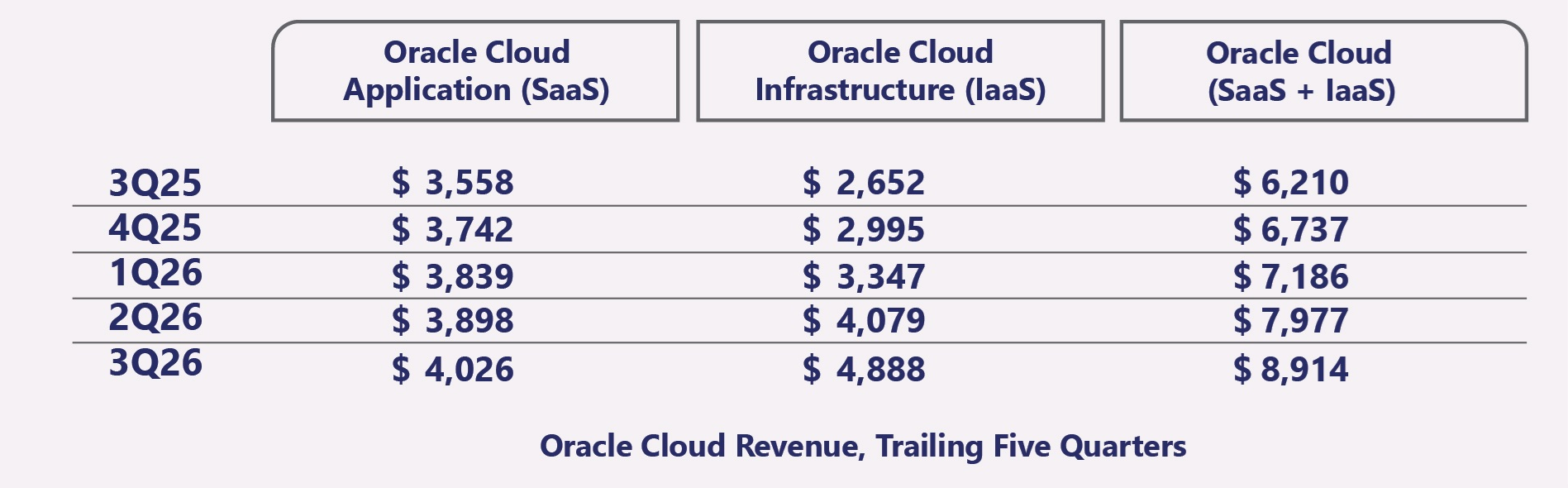

In fact, both its Oracle Fusion Cloud ERP Applications and NetSuite have been chalking up double-digit increases for the past 36 quarters without skipping a beat. For the latest quarter, the former rose 17% to $1.1 billion, while the latter gained 14% to reach $1.1 billion.

Its Cloud applications jumped 13% to exceed $4 billion in the latest quarter, up 11% in constant currency. By comparison, competitors like Salesforce and Workday saw high single-digit increases in their key products for CRM and HCM in recent quarters. Both Salesforce and Workday have continued with their buying spree with tucked-in purchases recently.

The second attribute that works to Oracle’s favor is its diversified offerings that touch every layer of the technology stack from database to apps and from hosting to AI training and inferencing.

Oracle Cloud Infrastructure (OCI), the late comer in the hyperscaler space, accelerated its growth in the latest quarter by chalking up an 84% jump in sales to reach $4.9 billion in the quarter. While still smaller than the hyperscaler operations at Amazon and Microsoft, Oracle’s ability to sign significant AI-infrastructure deals appears uncontested. The net gain of $29 billion in new orders – much of it attributed to OCI – during the three-month period has bolstered its remaining total obligations to a total $553 billion.

While it might be premature to write off many enterprise applications despite the stunning speed and performance of a growing cadre of AI training and inferencing tools that aim to rewire the workflows of every company with no assembly required through automatic coding and scripting directions from the likes of OpenAI, Anthropic and others, the breathtaking rollback of the tremendous software gain since the pandemic is evident.

Here again, investors appear to favor only a select few including Oracle. As shown in the following exhibit, Oracle is one of a handful of big techs that have seen at least 100% jump in their market capitalization since March 2021 when demand for tech issues appeared to be insatiable, a condition fanned by low interest rates, government stimuli and remote work benefits.

Triple-Digit-Plus Market Capitalization Gains Between March 2021 and March 2026

| Change in Market Cap Since March 2021 | |

|---|---|

| Alphabet | 199% |

| Apple | 107% |

| IBM | 103% |

| Meta | 109% |

| Nvidia | 1290% |

| Oracle | 134% |

Now as low interest rates become a distant memory and the ongoing $2-trillion private credit squeeze starts to eviscerate the borrowing capability of many privately-held software companies that are finding it harder to sustain their exorbitant sales and marketing machinery, one-hit wonders in the Cloud applications market have either seen their stocks crater or barely eke out a double-digit rise over the five-year period.

The simmering debate over whether Cloud apps vendors are going to be destroyed by the AI paradigm shift misses the point. Simply put, the pandemic rollback has made their predicament more vulnerable than ever, exacerbated by the fact that these best-of-breed providers are now being forced to play on somebody else’s terms.

Our research shows that with their silo approach, some of these vendors have not generated good visibility into their customers, or even worse fail to comprehend how their customers are running their applications at a granular level. That opens the door to data-miner and machine-learning operators like OpenAI and Anthropic.

The last thing that works to Oracle’s advantage is that its breadth of offerings now allows it to turn AI into a wedge issue, further gaining wallet shares at somebody else’s expense.

Case in point is Astris AI, a 15-month-old venture of giant federal contractor Lockheed Martin that is partnering with OCI, Meta and Nvidia to extend its domain expertise in security, aerospace and defense to high-assurance AI projects for both public and private-sector organizations.

OCI will deliver efficient and cost-effective cloud platform, enabling Astris to power its AI Factory MLOps and GenAI solutions for any organization that wants to scale out their AI initiatives rapidly and securely.

It comes as no surprise that Oracle will be able to cross-sell and upsell a slew of applications and infrastructure products to Astris AI and Lockheed Martin, which already standardizes on Oracle Fusion Cloud HCM for Core HR, while running Primavera and EPM for project management and planning.

Currently, Lockheed Martin has more than 80,000 enterprise users engaging with AI agents and digital assistants with over 20,000 GenAI agents deployed through a no-code platform, according to Astris executives, in addition to processing more than 13 billion tokens weekly with full compliance and auditability.

Harnessing such AI capabilities, Astris AI is now signing up utilities by helping them Improve grid reliability and resilience, boost clean energy innovation and strengthen cyber resilience.

If Oracle succeeds in flipping some of these enterprise accounts into applications wins after turning them into a captive audience with its OCI platform, it validates its contrarian position by calling AI threat a bluff. But the real lesson here is that the best-case scenario for Oracle to rebuke the demise of Cloud apps basically boils down to the cardinal rule of business – anyone can win provided it plays on its own terms.

Customer highlights from Oracle’s Q3 FY26 earnings