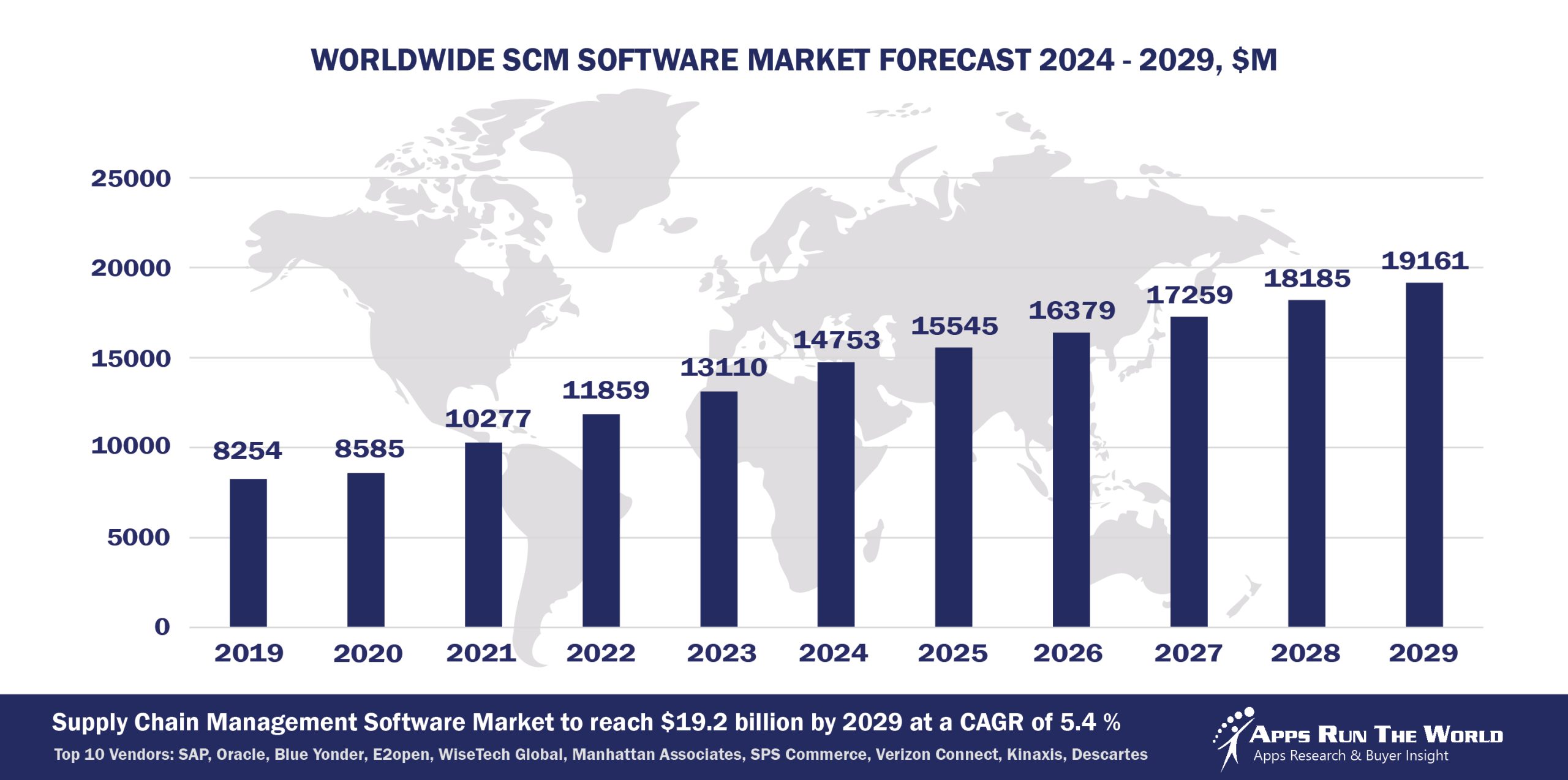

In 2024, the global Supply Chain Management (SCM) software market grew to $14.7 billion, marking a 12.5% year-over-year increase. The top 10 vendors accounted for 43.1% of the total market. SAP led the pack with a 12.2% market share, followed by Oracle, Blue Yonder, and E2open.

Through our forecast period, the SCM applications market size is expected to reach $19.2 billion by 2029, compared with $14.8 billion in 2024 at a CAGR of 5.4%, as shown in the Apps Top 500 Report – Excel Edition [Preview] .

Supply chain management covers Inventory Optimization (Warehouse Management, Replenishment), Transportation and Logistics (Routing, Scheduling, Carrier/Fleet/Fuel Management), Planning (Advanced Planning and Scheduling, Forecasting, Supply Chain Planning through Execution), Distribution Management (Order Orchestration, Management, Global Trade Management), E-Commerce (POS, Store Inventory & Fulfillment, EDI).

Internet of Things, global trade management are considered growth drivers, offset by retailing woes.

Top 10 SCM Vendors in 2024 and their Market Shares

Source: Apps Run The World, July 2025

Other SCM software providers included in the report are: abas Business Software, ABB, Access Group, Achilles, Adexa, Aera Technology, AFAS ERP Software, Aptean, Aptos, Arkieva, CDK Global, Comarch SoftM, Dematic, Emerson (inc. Aspen) , Epicor, ESM Solutions, Exact Holding BV, Exela Technologies, Famous Software, FOURGEN Information Systems, Fourth Ltd, FuturMaster, GAINSystems, Generix Group, GEP, GHX, HCL Technologies Ltd., IBM, IFS, Ignite Technologies, Intelex Technologies, iptor, Kinaxis Inc., Kingdee, Logility (ex American Software) Unite (Formerly Mercateo Group), NeoGrid, OM Partners, One Network Enterprises, Orgvue (formerly Concentra Analytics) ,ORTEC, Pitney Bowes, Pronto Software, QAD Inc., Quorum Software, Ramco Systems, Relex Solutions, River Logic, Inc., Roper Technologies, Sage, Sênior Sistemas, Slimstock, SupplyOn, Symphony RetailAI, Synchronoss, TechnologyOne Limited, Tecsys, Tigernix Pte Ltd, ToolsGroup, Tradeshift, Trimble, UNIT4, Veradigm (formerly Allscripts) Vizient, Vormittag Associates Inc., Yonyou, and others.

Vendor Snapshot: SCM Market Leaders

SAP

SAP

SAP has accelerated from advisory copilots toward fully autonomous agents embedded across its SCM stack—including SAP IBP, EWM, Transportation Management, and S/4HANA SCM. At Sapphire 2025, SAP unveiled a production-grade agent network powered by its AI Foundation and Joule Studio layered into SAP Business Suite. Agents like maintenance planner, dispatcher, and logistics supervisor can autonomously detect disruptions, enforce sustainability constraints, and trigger cross-domain workflows—from planning to procurement—via declarative, low-code definitions. The roadmap emphasizes conversational interfaces and citizen-developer tools that democratize autonomous supply chain orchestration.

Oracle

Oracle’s Fusion Cloud SCM suite (including Warehouse, Order, Transportation, Inventory, and Planning modules) now includes role-based AI agents as core operational stakeholders. In Release 24D, Oracle introduced fulfillment risk agents, sustainability advisors, policy bots, and maintenance guides that autonomously execute tasks using embedded policy logic, multilingual chat interfaces, and Fusion AI with OCI infrastructure. These agents now handle order orchestration, margin resilience, and compliance workflows end-to-end—with oversight and traceability—reflecting Oracle’s strategic shift toward unified, autonomous SCM operations.

Blue Yonder

Blue Yonder is embedding agentic AI directly into its Cognitive Solutions platform, powered by Snowflake, to deliver operational decisions at machine speed across planning, logistics, inventory, and returns. With its rollout of five domain-specific AI agents (Inventory, Warehouse, Logistics, Network, Shelf Operations), the vendor is automating real-time corrective actions and scenario modeling amid disruption. Sustainability is also built in via carbon‑aware decision support. This agentic-first architecture amplifies human-led planning and extends into low-code usage as business users refine workflows with conversational prompts and agents that act rather than just advise.

E2open

E2open’s transformation into an AI-native trade and logistics platform integrates agentic agents across its supply management, visibility, and compliance suites. Post-acquisition by WiseTech, the platform now includes agents that autonomously interpret unstructured documents, classify goods, manage trade validation, and execute compliance workflows. Its networked data architecture supports a low-code agent builder and conversational trade dashboards, empowering users to define agent roles and orchestrate trade flows across partners with no coding.

WiseTech Global

With its mid‑2025 acquisition of E2open, WiseTech is evolving into a unified agentic trade and logistics operating system using its CargoWise, Microlistics, and optimization platforms. This combined architecture allows autonomous agents to span global transport, visibility, procurement, and compliance. The roadmap includes low-code orchestration interfaces for configuring multi-agent coordination—setting the direction toward intelligent logistics automation across multi-enterprise supply chains.

Manhattan Associates

At Momentum 2025, Manhattan unveiled LLM‑powered agents embedded within its cloud-native Active platform (WMS, Transportation, Supply Chain, Order Management, Inventory, and Scale products). These agents autonomously handle order orchestration, labor planning, fulfillment routing, and demand sensing. The Agent Foundry feature enables citizen developers to configure tailored agents using conversational interfaces and workflow triggers—supporting agile supply chain operations that adapt dynamically to real-world variability.

SPS Commerce

SPS Commerce, operating at the backbone of retail trading networks, is experimenting with AI-driven analytics agents that parse EDI transactions and retail data to automate exception detection, demand forecasting, and inventory insights. While still early in agentic transition, the roadmap now previews conversational dashboards and automated workflows driven by embedded agents that alert, explain, and recommend resolutions, paving a path toward end‑to‑end retail supply chain agents in future releases.

Verizon Connect

Verizon Connect is positioning its Verizon AI Connect platform—running on private 5G infrastructure at logistics hubs like Thames Freeport—as a backbone for agentic logistics orchestration. Though at early stages, its roadmap includes edge-deployed agents for predictive routing, autonomous dispatch, and context-aware route optimization via conversational interfaces for drivers and dispatchers. This vision combines real‑time sensing with agentic decisioning at the network edge to optimize fleet operations end-to-end.

Kinaxis

Kinaxis’s Maestro platform (including Planning One, Demand, Inventory, and Order modules) now houses a unified “Planning.AI Fusion” layer that blends optimization, heuristics, and autonomous re-planning. At Kinexions 2025, Kinaxis announced its new agentic AI framework, built on Databricks, which lets citizen developers create supply chain agents via natural language—such as agents that detect shortages or rebalance supply in seconds rather than hours. This dual human‑AI oversight model reinforces Kinaxis’s focus on proactive, resilient planning.

Descartes Systems Group

Descartes continues to leverage its Global Logistics Network, now used by over 24,000 logistics-intensive businesses globally, to drive AI‑infused insight across transportation, global trade, customs, and compliance workflows. These agents reduce false positives in denied-party lists, automate trade classification, and provide conversational multilingual trade compliance interfaces. Deployed globally, this shift represents a transition from rule-based workflows to agent-assisted trade intelligence that supports seamless, compliant cross-border logistics at scale.

ARTW Technographics Platform: SCM customer wins

Since 2010, our research team has been studying the patterns of the SCM software purchases, analyzing customer behavior and vendor performance through continuous win/loss analysis. Updated quarterly, the ARTW Technographics Platform provides deep insights into thousands of SCM customer wins and losses, helping users monitor competitive shifts, evaluate vendor momentum, and make informed go-to-market decisions.

List of SCM customers

Source: ARTW Buyer Insights Technographic Database

Custom data cuts related to the SCM Applications market are available:

- Top 250+ SCM Applications Vendors and Market Forecast 2024-2029

- 2024 SCM Applications Market By Industry (21 Verticals)

- 2024 SCM Applications Market By SCM Segments and Categories

- 2024 SCM Applications Market By Country (USA + 45 countries)

- 2024 SCM Applications Market By Region (Americas, EMEA, APAC)

- 2024 SCM Applications Market By Revenue Type (License, Services, Hardware, Support and Maintenance, Cloud)

- 2024 SCM Applications Market By Customer Size (revenue, employee count, asset)

- 2024 SCM Applications Market By Channel (Direct vs Indirect)

- 2024 SCM Applications Market By Product

Worldwide Enterprise Application Market

Exhibit 3 provides a forecast of the worldwide enterprise application market from 2024 to 2029, highlighting market sizes, year-over-year growth, and compound annual growth rates across various functional segments. The data shows strong growth in emerging areas like Content Management, eCommerce, Human Capital Management, and IT Service Management, while traditional segments like ERP and CRM continue to dominate in market size.

Exhibit 3: Worldwide Enterprise Application Market Forecast 2024-2029 by Functional Market, $M

Source: Apps Run The World, July 2025

Exhibit 4 shows the enterprise applications market by functional area. The highest growth functional markets revolve around smaller segments like Analytics and BI, eCommerce, Enterprise Performance Management, where first movers remain less established than those that for decades have been entrenched in functional areas like ERP, HCM, CRM and PLM.

FAQ – APPS RUN THE WORLD Top 10 Supply Chain Management Software Vendors, Market Size & Forecast

Q1. What is the global SCM software market size in 2024?

A: The global SCM software market was $14.7 billion in 2024, growing 12.5% year-over-year.

Q2. Who are the top 10 SCM software vendors in 2024, and what share do they hold?

A: The top 10 vendors are SAP, Blue Yonder, Manhattan Associates, Oracle, Infor, Coupa, Kinaxis, Epicor, E2open, and Dassault Systèmes, together accounting for 43.1% of the SCM market.

Q3. Which vendor leads the SCM software market in 2024?

A: SAP leads the SCM market with approximately 12.2% market share.

Q4. What is the forecast for the SCM software market through 2029?

A: The SCM applications market is expected to reach $19.2 billion by 2029, growing at a 5.4% compound annual growth rate (CAGR).

Q5. What functions are included in the scope of SCM in this report?

A: The report covers inventory optimization, transportation & logistics, planning (forecasting & execution), distribution management (order orchestration and global trade), and e-commerce fulfillment.

Q6. Which other SCM software vendors are covered beyond the top 10?

A: The report also profiles vendors such as JDA Software, Manhattan Associates, Epicor, Infor, and Kinaxis, among others.

Q7. When was this SCM report published and by whom?

A: The Top 10 SCM Software Vendors, Market Size & Forecast 2024–2029 report was published in July 2025 by APPS RUN THE WORLD analysts Albert Pang, Misho Markovski, and Jasmina Ristovska, as part of the APPS TOP 500 research program, which benchmarks the revenues and market share of the world’s 1,500+ largest enterprise application vendors.

More Enterprise Applications Research Findings

Based on the latest annual survey of 10,000+ enterprise software vendors, Apps Run The World is releasing a number of dedicated reports, which profile the world’s 1,500 largest Enterprise Applications Vendors ranked by their 2024 product revenues. Their 2024 results are being broken down, sorted and ranked across 16 functional areas (from Analytics and BI to Treasury and Risk Management) and by 21 vertical industries (from Aerospace to Utility), as shown in our Taxonomy. Further breakdowns by subvertical, country, company size, etc. are available as custom data cuts per special request.

Research Methodology

Each year our global team of researchers conduct an annual survey of thousands of enterprise software vendors by contacting them directly on their latest quarterly and annual revenues by country, functional area, and vertical market.

We supplement their written responses with our own primary research to determine quarterly and yearly growth rates, In addition to customer wins to ascertain whether these are net new purchases or expansions of existing implementations.

Another dimension of our proactive research process is through continuous improvement of our customer database, which stores more than one million records on the enterprise software landscape of over 2 million organizations around the world.

The database provides customer insight and contextual information on what types of enterprise software systems and other relevant technologies are they running and their propensity to invest further with their current or new suppliers as part of their overall IT transformation projects to stay competitive, fend off threats from disruptive forces, or comply with internal mandates to improve overall enterprise efficiency.

The result is a combination of supply-side data and demand-generation customer insight that allows our clients to better position themselves in anticipation of the next wave that will reshape the enterprise software marketplace for years to come.

- Polsia, a United States based Professional Services organization with 10 Employees

- Mindtree Consulting (LTI Mindtree), a India based Professional Services company with 83000 Employees

- SS Supply Chain Solutions 3SC, a India based Professional Services organization with 200 Employees

| Logo | Company | Industry | Employees | Revenue | Country | Evaluated |

|---|