As artificial intelligence is fast becoming the mother of all markets for technology providers, there are clear signs that customer appetite may be working against the same vendors that espouse all things AI.

Following our annual survey of thousands of enterprise software vendors and their customers over the past few months, ARTW has released a slew of market-sizing reports that detail the latest status and forecast of every possible segment from ERP software for general enterprise to domain-specific products for dozens of vertical industries.

Software vendors now find themselves navigating the treacherous terrains by riding the AI wave while sustaining their core offerings at the same time. Similar to previous paradigm shifts, software is a few steps behind hardware, specifically semiconductors in this case.

That has benefited chip makers like Nvidia, which is now considered the motherlode of enterprise IT spend, having become the chief beneficiary of the AI hype due to its popular chipsets that facilitate large language modeling at scale, while capitalizing on its status as the world’s most valuable company.

Exhibit 1 breaks down the Enterprise IT spend by category over the next five years as ARTW includes hardware server and semiconductor, both of which are deemed to be essential to the future of enterprise computing.

Exhibit 1 – Worldwide Enterprise IT Spend Market Size and Forecast 2024-2029, $B and CAGR, %

As shown in the CAGR of different enterprise IT categories, lavish spending on Infrastructure As A Service, coupled with semiconductors, is likely to propel both to achieve double-digit growth through 2029.

Trade disputes, geopolitical conflicts and speculative investors notwithstanding, how software vendors can profit from AI depends on their ability to assess risk. In short, risk has become so concentrated and its profile more circular than ever, meaning that risk could feed on itself to multiply the rewards and potentially afflict significant damage in a stunning about-face. For reality check, one needs to look no further than the Dot Com bust in 2000, financial crisis in 2008 and the associated casualties from Enron to Webvan.

In Nvidia’s latest second quarter of fiscal 2026, two customers accounted for 39% of its revenue. After all, only a handful of customers can afford to buy in bulk its H100 chip priced between $27,000 and $40,000 for meaningful AI developments. In fact, Nvidia is planning to invest up to $100 billion in OpenAI in order to sustain the operations of one of its biggest customers.

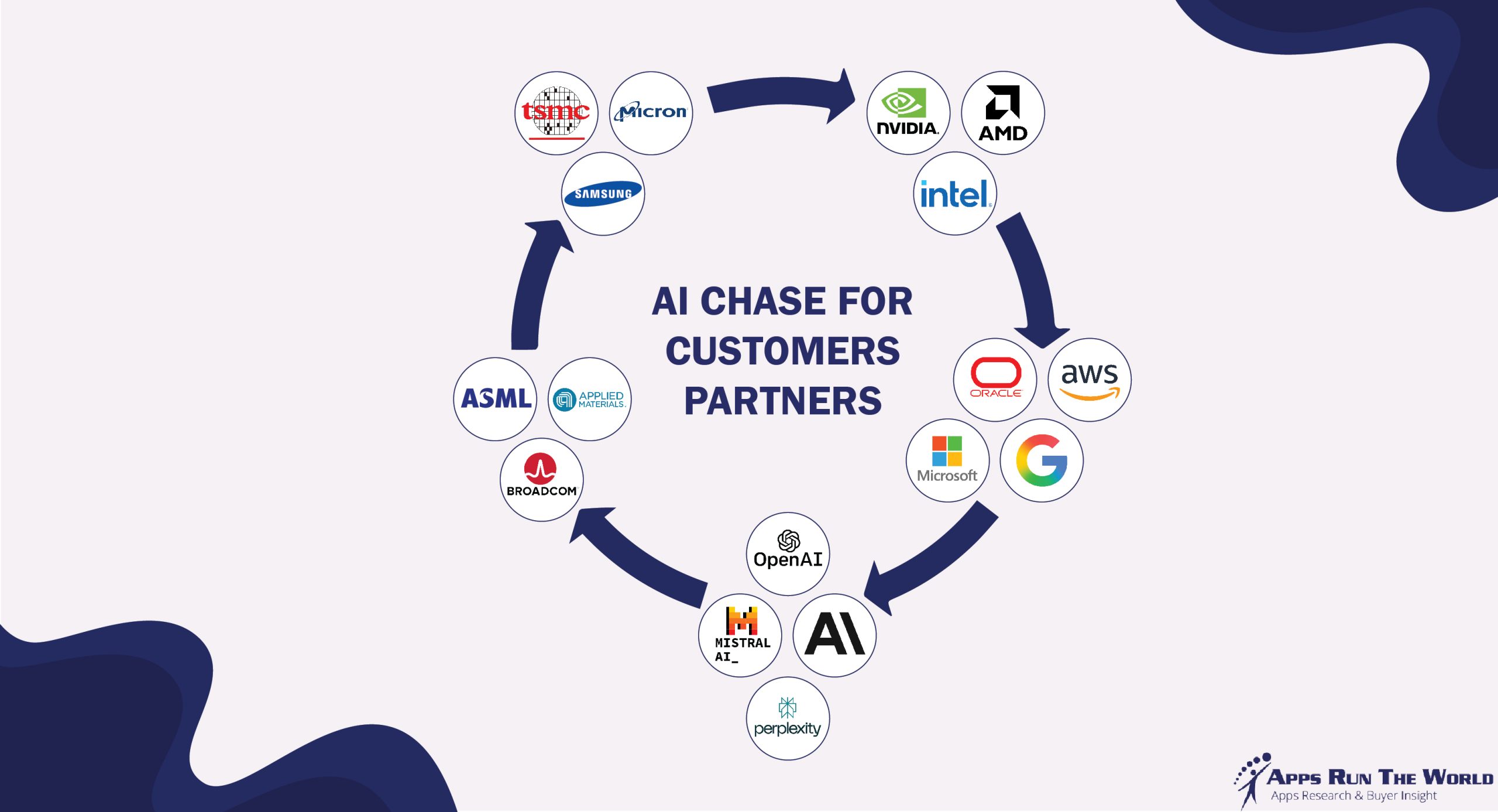

Exhibit 2 shows just how circular the AI chase has become with some vendors relying on a few customers for a big chunk of their revenues.

Upping the ante, major vendors have evolved their AI strategies in order to mitigate or further concentration risk depending on how this game of chicken is going to play out.

In September 2025, Microsoft signed a $17 billion deal with Nvidia-backed Nebius, which will provide AI infrastructure and modeling work for Azure users through 2031. Microsoft also relies on CoreWeave and OpenAI for similar developments.

The same month, ASML, the semiconductor company that puts lithography onto silicon wafers for other chip makers including TSMC, invested $1.5 billion for an 11% stake in Mistral, a French AI startup that aims to leapfrog OpenAI and Anthropic in large language modeling.

The sense of urgency is unmistakable. When Oracle announced its latest earnings in September, its remaining performance obligations, or revenues to be booked, more than quadrupled to a record of $455 billion, much of it was attributed to its Oracle Cloud Infrastructure business from CEOs, heads of states and a cluster of AI logos from OpenAI to Stargate wanting to use its Cloud platform for rapid AI inferencing.

Because of the surge of AI inferencing interest, Oracle CEO Safra Catz projected that its OCI revenues to exceed $144 billion by the end of the decade, compared with $18 billion in its current fiscal year.

Customer Sentiment Check

The optimistic outlook stands in contrast to a litany of recent studies and rebuttals questioning whether vendors and customers can easily and quickly derive real benefits from pivoting to AI. That includes an August 2025 study from MIT citing 95% of generative AI pilots at companies are failing.

A more likely outcome is that if companies are investing so much on Gen AI inferencing, they could be left with no choice but to slash other existing and ongoing IT projects, not to mention eliminating other personnel and administrative expenses that would be written off as redundancy under the broad digital transformation umbrella.

In one of our latest surveys of enterprise customers this year that involved 104 IT executives including 23 chief information officers and IT heads from some of the biggest organizations such as Grupo Bimbo, Salesforce, and Wells Fargo Bank in nine countries. The top priorities for enterprise buyers over the next 12 to 24 months are leveraging AI enhancements with 63% of the respondents, and reducing operating and support costs cited by 54% of these key stakeholders.

That is consistent with the user sentiment commonly shared by leading organizations. In an August 2025 piece in the Wall Street Journal, Bank of America Chief Technology and Information Officer Hari Gopalkrishnan, said the bank plans to invest as much as $4 billion in new technologies like AI out of a total technology budget of $13 billion this year.

That sounds like a rich sum, but BOA chief executive Brian Moynihan was quoted as saying in its Q3 2023 earnings call that it would be spending $3.8 billion on innovation – most likely involving AI – in 2024 out of a total IT budget $12 billion.

In other words, the IT budget at BOA has risen about 8% from $12 billion in 2023 to $13 billion in 2025, or about 4% per year. During that period, BOA’s revenues rose 3.3% from 2023 to 2024 and its current run rate is showing a 5% increase in sales for the first half of 2025. That appears to be a right direction for a big entity that continues to chalk up improving results.

What is left unsaid is the fact that Bank of America used to operate an IT budget of as much as $16 billion prior to the pandemic and it has been cutting costs by closing many data centers.

Peaking of IT Budget

When it comes to enterprise IT spend, budget has peaked for many buyers. In a recent survey of utilities in the United States, many have reported reducing their IT spending.

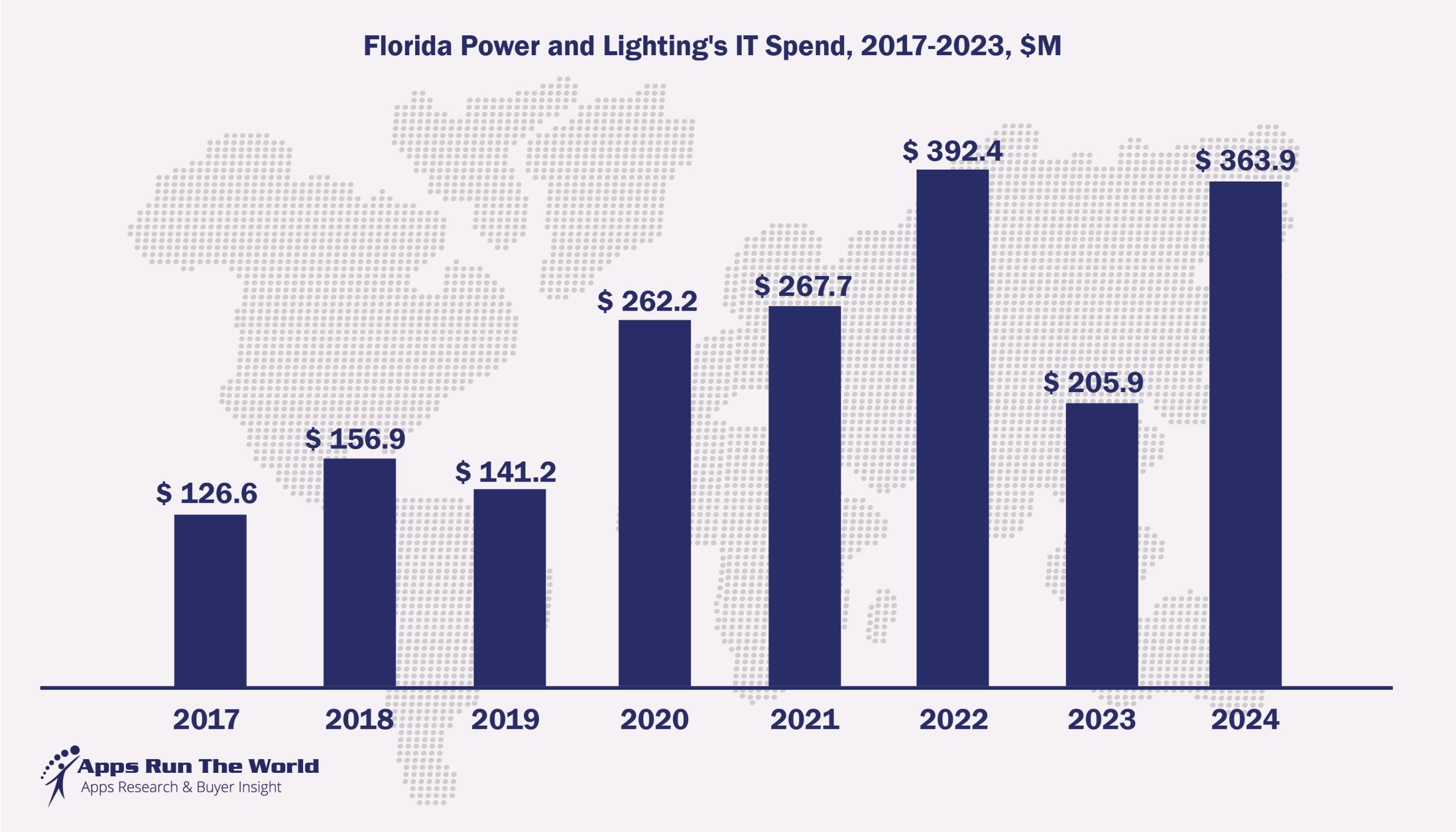

Such belt-tightening moves are evident at energy providers like Florida Power and Light Company, which filed with the Federal Energy Regulatory Commission every year by documenting its IT spend, which has tumbled from $392 million at its peak in 2022 to $364 million in 2024, as shown in the following exhibit.

Exhibit 3 – Florida Power and Lighting’s IT Spend, 2017-2023, $M

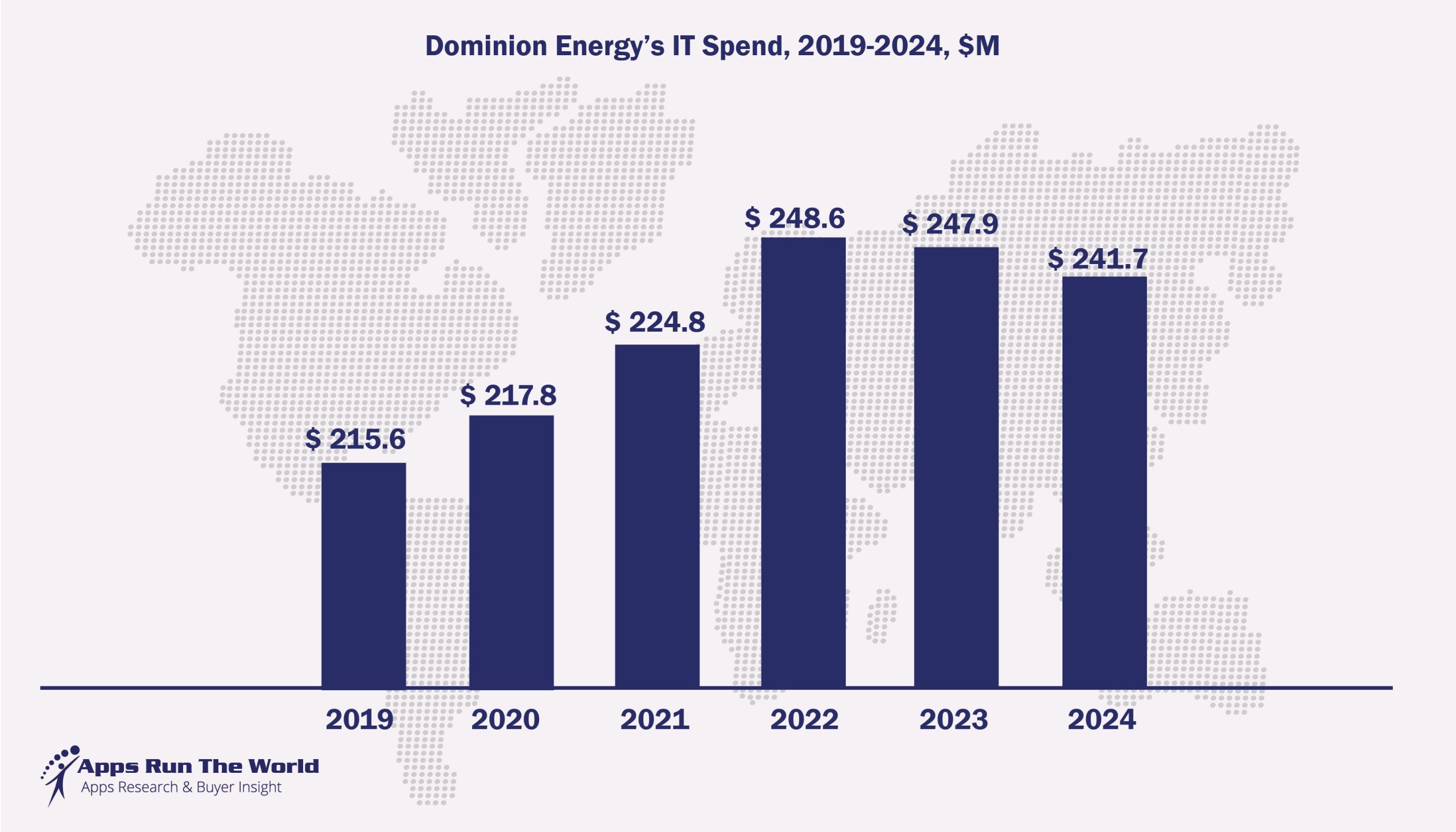

At Dominion Energy in Virginia which houses some of the world’s biggest data centers that consume staggering amount of electricity, the same cutbacks are evident. Its total IT spend amounted to $248.6 million in 2022 at its peak and it has been slipping to $241.7 million in 2024, as shown in the following exhibit.

Exhibit 4 – Dominion Energy’s IT Spend, 2019-2024, $M

For every BOA, FP&L, or Dominion Energy that is going to be investing in cutting-edge AI projects, chances are something else has to give. The implication is that many enterprise software vendors are now struggling to position themselves as AI-centric, while resolving the fact that some parts of their business will be adversely impacted.

The massive reconfiguration of the enterprise software market is beginning to take shape. Here are some of the recent examples:

Both Verint in call center applications and Dayforce for HCM software have been taken private at prices far below their peaks over the past few years. The September 2025 sale of Pros Holdings for pricing optimization software to Thoma Bravo followed the same pattern.

Genesys, another call center apps provider, has attracted $1.5 billion in fresh capital from Salesforce and ServiceNow, which will be co-selling and distributing some of their products to the installed base of the CX vendor.

Other enterprise software vendors have fared much worse. Since March 2025, CareerBuilder + Monster, Digital River, Exela Solutions, and Marin Software have all filed for bankruptcy.

On the other hand, Ramp for travel and expense management raised $500 million for its AI-powered finance applications in July 2025, while Egnyte for content management, Think-cell for Powerpoint add-on and ArcticDB for Excel-like capabilities have garnered rapid adoptions with their AI-powered tools.

Even OpenAI is trying to crack the office productivity market with the introduction of agents that mimic presentation and spreadsheet capabilities through ChatGPT.

While the public is still waiting for the arrival of killer AI applications, the enterprise software market will see barriers that separate some of these functional areas like interactive voice response, customer service and support or content management coming down and many of the vendors involved barging into each other’s territories such as the convergence of HR and Collaboration if they do not want to be roadkill.

Enterprise Software Market Outlook

With the advent of AI modeling, inferencing and agents working around the clock, the enterprise software market will never look the same. Here are some of the new rules that vendors, partners and customers must take note:

As discussed in these reports before, a successful tech company needs to have three elements – data, widget and customer experience that appeal to buyers. That pretty much sums up the story behind iPhone.

Regardless of the impact of generative AI, that truism will also matter. Because of the pace of change, one must size up AI competition on a real-time basis to determine if they are for real or for nought.

Companies need to benchmark themselves constantly against their peers and others that come into their universe, certainly with the highest-quality data repository they can get their hands on.

That leaves us with the question of whether data sharing in the age of Generative AI is permissible. It is a pact with the devil if a company chooses to share certain data sets for AI training, modeling and inferencing. Our advice is that it will have to be a two-way street guaranteeing users something tangible back in return.

The age of AI is full of irony when vendors like Salesforce and ServiceNow are partnering to carve up Genesys’ installed base at the same time when they are at each other’s throat. The same applies to Oracle competing and partnering with AWS, Google and Microsoft simultaneously.

This underscores the fact that one’s definition of risk is opportunity for another. Taking a more conservative stance than these mega vendors that have the more resources to cushion the blow, the real gamechanger for the rest may require standing back a tiny bit, fully assessing the risk profile of all the parties involved and then spreading their bet around judiciously since everybody is doing exactly the same. Returns may be more modest, so will the collateral damage.

The only fear is not to take AI seriously, but one should never refrain from staring down its competition with focus, a clear mission, and hopefully plenty of solid and accurate data at one’s disposal to execute flawlessly.

Worldwide Enterprise Application Market

Exhibit 5 provides a forecast of the worldwide enterprise application market from 2024 to 2029, highlighting market sizes, year-over-year growth, and compound annual growth rates across various functional segments. The data shows strong growth in emerging areas like eCommerce, Human Capital Management, and IT Service Management, while traditional segments like ERP and CRM continue to dominate in market size.

This exhibit shows the enterprise applications market by functional area. The highest growth functional markets revolve around smaller segments like eCommerce, Enterprise Performance Management, Sales Performance Management and Treasury and Risk, where first movers remain less established than those that for decades have been entrenched in functional areas like ERP, CRM and PLM.

Worldwide Enterprise Application Market Forecast 2024-2029 by Vertical Market, $M

Exhibit 7 provides a forecast of the worldwide enterprise applications by vertical market from 2024 to 2029, highlighting market sizes, year-over-year growth, and compound annual growth rates across different industry sectors from Aerospace and Defense to Utilities.

Exhibit 8 shows our projections for the enterprise applications market by vertical segment, based on the buying preferences and the customer propensity to invest in new software within those industries as they continue to upgrade and replace many legacy industry-specific applications that have been identified and tracked in our Buyer Insight Database.

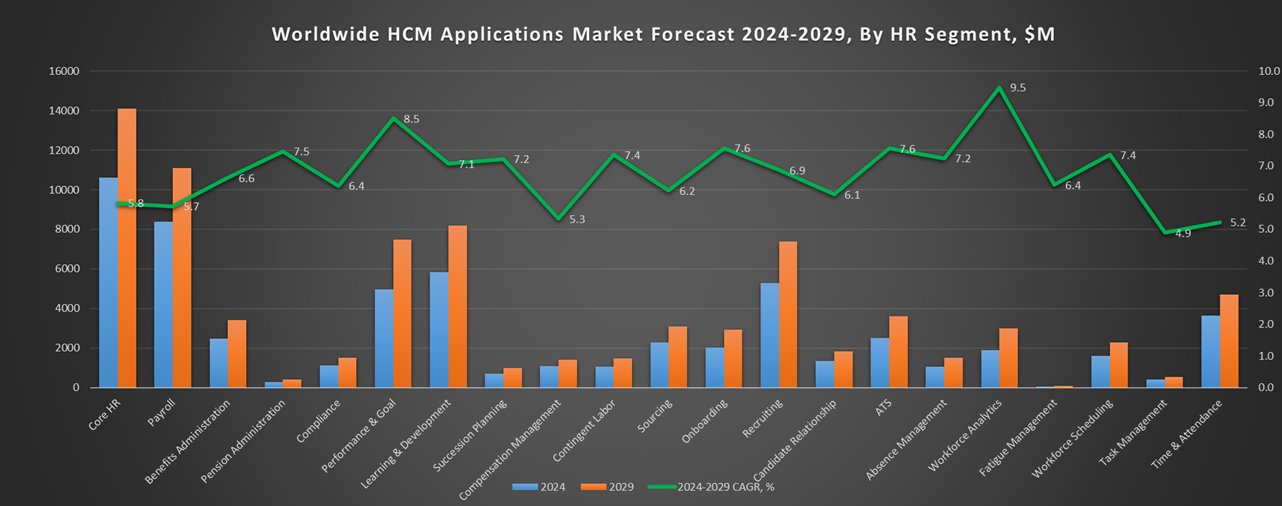

Worldwide HCM Software Market Forecast 2024-2029 by HR Segments, $M

Through our forecast period, the HCM applications market is expected to reach $81.1 billion by 2029, compared with $58.7 billion in 2024 at a compound annual growth rate of 11.7%.

Through our forecast period, the Core HR and Talent Management applications market, which is comprised of nine subsegments, is expected to reach $48.6 billion by 2029, compared with $35.5 billion in 2024 expanding at a compound annual growth rate of 11.6%. For the Top 10 vendors in each of the nine subsegments, please check their own index page by following the link below.

Through our forecast period, the Talent Acquisition applications market, which is comprised of six subsegments, is expected to reach $20.3 billion by 2029, compared with $14.5 billion in 2024 expanding at a compound annual growth rate of 11.7%. For the Top 10 vendors in each of the six subsegments, please check their own index page by following the link below.

Through our forecast period, the Workforce Management applications market, which is comprised of six subsegments, is expected to reach $12.1 billion by 2029, compared with $8.7 billion in 2024 expanding at a compound annual growth rate of 12.1%. For the Top 10 vendors in each of the six subsegments, please check their own index page by following the link below.

Our HCM Top 500 research team also tracks Time Clock Hardware vendors separately by zeroing in on their embedded software as well as their extensive use of OEM and distribution partners.

The exhibit below shows our projections for the HCM enterprise applications market by HCM sub-segment, based on the buying preferences and the customer propensity to invest in new software within those industries as they continue to upgrade and replace many legacy industry-specific applications that have been identified and tracked in our Buyer Insight Database.

Worldwide HCM Applications Market Forecast 2024-2029, By HR Segments, $M

Research Methodology

Each year our global team of researchers conduct an annual survey of thousands of enterprise software vendors by contacting them directly on their latest quarterly and annual revenues by country, functional area, and vertical market.

We supplement their written responses with our own primary research to determine quarterly and yearly growth rates, In addition to customer wins to ascertain whether these are net new purchases or expansions of existing implementations.

Another dimension of our proactive research process is through continuous improvement of our customer database, which stores more than one million records on the enterprise software landscape of over 2 million organizations around the world.

The database provides customer insight and contextual information on what types of enterprise software systems and other relevant technologies they are running and their propensity to invest further with their current or new suppliers as part of their overall IT transformation projects to stay competitive, fend off threats from disruptive forces, or comply with internal mandates to improve overall enterprise efficiency.

The result is a combination of supply-side data and demand-generation customer insight that allows our clients to better position themselves in anticipation of the next wave that will reshape the enterprise software marketplace for years to come.

2025 Enterprise Applications, IaaS, PaaS and AI Customer Wins and Digital Transformation Initiatives

Source: APPS RUN THE WORLD Technographics Platform, September 2025

Buyer Intent: Companies Reading this Research Report

ARTW Buyer Intent uncovers actionable customer signals, identifying software buyers actively reading this research report. Gain ongoing access to real-time prospects and uncover hidden opportunities. Companies Actively accessing this research report include:

Weston Nurseries, a United States based Retail organization with 20 Employees

Uber, a United States based Transportation company with 31100 Employees

KPMG, a Netherlands based Professional Services organization with 273424 Employees